As filed with the Securities and Exchange Commission on March 30, 2021

Registration No. 333-254235

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| GEE GROUP INC. |

| (Exact name of registrant as specified in its charter) |

| Illinois |

| 7361 |

| 36-6097429 |

| (State or other jurisdiction of |

| (Primary standard industrial |

| (I.R.S. employer |

GEE Group Inc.

7751 Belfort Parkway, Suite 150

Jacksonville, Florida 32256

(630) 954-0400

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Derek E. Dewan

Chief Executive Officer

GEE Group Inc.

7751 Belfort Parkway, Suite 150

Jacksonville, Florida 32256

(630) 954-0400

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| Mitchell S. Nussbaum, Esq. Loeb & Loeb LLP | Oded Har-Even, Esq. Angela Gomes, Esq. Sullivan & Worcester LLP 1633 Broadway New York, NY 10019 Tel: (212) 660-3000 Fax: (212) 660 3001 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

|

|

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Security Being Registered |

| Proposed Maximum Aggregate Offering Price(1) (2) |

|

| Amount of Registration Fee(3) |

| ||

| Common Stock, no par value |

| $ | 57,500,000 |

|

| $ | 6,273.25 |

|

| Total |

| $ | 57,500,000 |

|

| $ | 6,273.25 |

|

| (1) | Includes additional shares of common stock that may be issued upon exercise of a 45-day option granted to the underwriters to cover over-allotments, if any. |

|

|

|

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

|

|

|

| (3) | Previously Paid. Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price of the securities registered hereunder to be sold by the registrant, and includes the offering price of shares of common stock that the underwriters have an option to purchase to cover over-allotments, if any. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

| 2 |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS |

| SUBJECT TO COMPLETION |

| DATED MARCH 29, 2021 |

31,250,000 Shares

Common Stock

| GEE Group Inc. |

We are offering 31,250,000 shares of our common stock, no par value, at an assumed public offering price of $1.60 per share, the last reported sale price of our common stock on the NYSE American on March 26, 2021. The final public offering price of the shares of common stock being offered in this offering will be determined through negotiation between us and the underwriters in this offering and the last reported sale price of our common stock used throughout this prospectus may not be indicative of the final offering price.

Our common stock is listed on the NYSE American under the symbol “JOB.” On March 26, 2021, the closing price of our common stock on the NYSE American was $1.60 per share.

Investing in our securities involves a high degree of risk, including that the trading price of our common stock has been subject to volatility and investors in this offering may not be able to sell their common stock above the actual offering price or at all. Before making any investment decision, you should carefully review and consider all the information in this prospectus, including “Risk Factors” beginning on page 18 of this prospectus and the risk factors incorporated herein by reference into this prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

|

| Per Share |

| Total | |||

| Public offering price |

| $ |

| $ |

| ||

| Underwriting discounts and commissions(1) |

| $ |

|

| $ |

|

|

| Proceeds to us, before expenses |

| $ |

|

| $ |

|

|

_______________________________________

(1) We have agreed to pay the underwriters a cash fee equal to 7.5% of the gross proceeds raised in this offering, and to reimburse certain of their offering-related expenses. See “Underwriting” for additional information regarding underwriting compensation.

We have granted a 45-day option to the underwriters to purchase up to additional shares of our common stock solely to cover over-allotments, if any.

The underwriters expect to deliver the shares of common stock to purchasers on or about ____________ , 2021.

ThinkEquity

a division of Fordham Financial Management, Inc.

The date of this prospectus is __________ , 2021

| 3 |

|

|

|

|

| 4 |

|

|

|

| Page |

|

|

|

|

|

|

|

|

|

| 7 |

| |

|

|

| 16 |

| |

|

|

| 17 |

| |

|

|

| 19 |

| |

|

|

| 35 |

| |

|

|

| 36 |

| |

|

|

| 36 |

| |

|

|

| 37 |

| |

|

|

| 38 |

| |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

|

| 39 |

|

|

|

| 58 |

| |

|

|

| 65 |

| |

|

|

| 67 |

| |

|

|

| 74 |

| |

|

|

| 74 |

| |

|

|

| 74 |

| |

|

|

| 75 |

| |

|

| F-1 |

|

| 5 |

We and the underwriters have not authorized anyone to provide you any information other than that contained in this prospectus, the documents incorporated by reference herein or in any free writing prospectus prepared by or on behalf of us or to which we have referred you, and you should rely only on the information contained in this prospectus, the documents incorporated by reference herein or in any such free writing prospectus. In addition, this prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under the heading “Where You Can Find More Information.” Information contained in later-dated documents incorporated by reference will automatically supplement, modify or supersede, as applicable, the information contained in this prospectus or in earlier-dated documents incorporated by reference.

We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are not making an offer to sell nor a solicitation of any offer to buy these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus, the documents incorporated by reference herein and any applicable free writing prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside of the United States: we have not and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside of the United States.

Our logo and some of our trademarks and tradenames are used or incorporated by reference in this prospectus. This prospectus also includes trademarks, tradenames and service marks that are the property of other organizations. Solely for convenience, trademarks, tradenames and service marks referred to in this prospectus may appear without the ®, TM and SM symbols, but those references are not intended to indicate in any way that we will not assert to the fullest extent under applicable law our rights or the rights of the applicable licensor to these trademarks, tradenames and service marks.

We obtained the statistical data, market data and other industry data and forecasts described or incorporated by reference in this prospectus from market research, publicly available information and industry publications. Industry publications generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy and completeness of the information. Similarly, while we believe that the statistical data, industry data and forecasts and market research are reliable, we have not independently verified the data, and we do not make any representation as to the accuracy of the information. We have not sought the consent of the sources to refer to their reports appearing or incorporated by reference in this prospectus.

As used in this prospectus, unless the context indicates or otherwise requires, “the Company,” “our company,” “we,” “us,” and “our” refer to GEE Group Inc. and its subsidiaries taken as a whole.

This prospectus is an offer to sell only the securities offered hereby, and only under circumstances and in jurisdictions where it is lawful to do so. We are not, and the underwriters are not, making an offer to sell these securities in any state or jurisdiction where the offer or sale is not permitted.

| 6 |

| Table of Contents |

This summary highlights information contained in other parts of this prospectus or incorporated by reference into this prospectus from our filings with the Securities and Exchange Commission (the “SEC”) listed in the section of the prospectus entitled “Information Incorporated by Reference.” Because it is only a summary, it does not contain all of the information that you should consider before purchasing our securities in this offering and it is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere or incorporated by reference into this prospectus. You should read the entire prospectus, the registration statement of which this prospectus is a part, and the information incorporated by reference herein in their entirety, including the “Risk Factors” and our audited and unaudited consolidated financial statements and the related notes incorporated by reference into this prospectus, before making an investment decision. Some of the statements in this prospectus and the documents incorporated by reference herein constitute forward-looking statements that involve risks and uncertainties. See information set forth under the section “Cautionary Note Regarding Forward-Looking Statements.”

Our Company

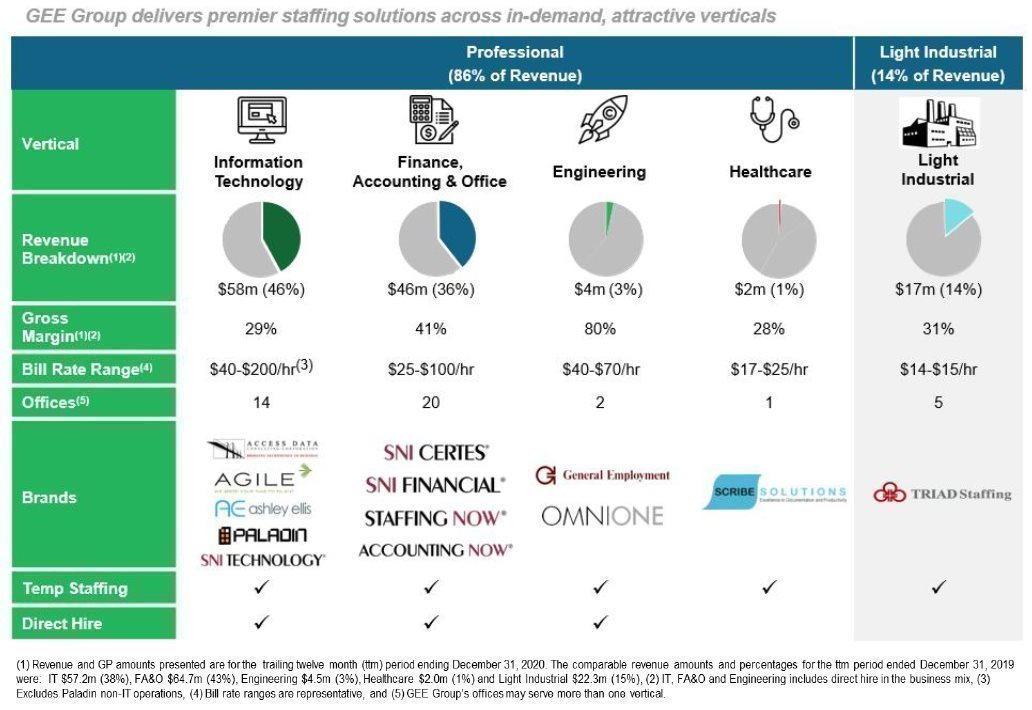

We are a provider of human resources solutions which primarily include the provision of temporary and permanent personnel in the professional and industrial services sectors to customers located throughout the United Sates. We, through our operating subsidiaries, deliver our services from a network of three virtual locations and 27 branch office locations located in or near several major U.S. cities, including, but not limited to, Atlanta, Dallas, Denver and Miami. We specialize primarily in the placement of information technology (“IT”), engineering, accounting and finance, health care, including medical assistants (“scribes”) who specialize in electronic medical records (“EMR”) services for emergency departments, specialty physician practices and clinics, and office support professionals for direct hire and contract staffing. We also provide temporary light industrial (blue collar) staffing services for commercial clients.

Our material operating subsidiaries include Access Data Consulting Corporation, Agile Resources, Inc., BMCH, Inc., Paladin Consulting, Inc., Scribe Solutions, Inc., SNI Companies, Inc., Triad Logistics, Inc., and Triad Personnel Services, Inc. In addition, we and our operating subsidiaries own and operate under other trade names, including Accounting Now, Ashley Ellis, Staffing Now®, SNI Banking, SNI Certes®, SNI Energy®, SNI Financial®, SNI Technology®, GEE Group (Columbus), General Employment, Omni One and Triad Staffing.

Services Provided

We provide our services to a broad range of customers from small and medium-sized businesses to the Fortune 1000. Our services include the provision of highly specialized contract or permanently placed professionals in several verticals, including IT, engineering, accounting and finance, office support and healthcare, including scribes who specialize in EMR services for emergency departments, specialty physician practices and clinics. We provide office support professionals for direct hire and contract staffing. We also provide temporary staffing services in the light industrial (blue collar) areas.

Our contract and placement services are principally provided under two operating divisions or segments: Professional Staffing Services and Industrial Staffing Services.

Our operating subsidiaries and end markets served under each of our operating divisions are as follows:

Professional Division

|

| · | Access Data Consulting provides hard-to-find IT talent to customers on a direct hire or contract basis and human resources consulting services and solutions in the higher-end IT vertical including project management support to businesses regionally (Western and Southwestern U.S.) and, to a lesser extent, throughout the rest of the U.S. |

|

|

|

|

|

| · | Agile Resources delivers unique Chief Information Officer (“CIO”) advisory services, IT project support and human resources solutions regionally (Southeastern U.S.) and, to a lesser extent, nationally in the areas of application architecture and delivery, enterprise operations, digital, information lifecycle management and project management all with flexible delivery options including contract staffing and direct hire. |

| 7 |

| Table of Contents |

|

| · | Ashley Ellis works with C-suite and senior executives to offer full cycle engineering and IT contract staffing services, with a focus on business intelligence, application development and network infrastructure, to clients in the Southeastern U.S. region and, to a lesser extent, throughout the rest of the U.S. |

|

|

|

|

|

| · | GEE Group (Columbus) primarily provides direct hire placement and contract staffing services in the accounting and engineering verticals, with an emphasis on placing personnel with specialized skills in the mechanical, manufacturing and equipment maintenance areas to clients throughout the Midwestern U.S. |

|

|

|

|

|

| · | Omni One specializes in technical and professional direct-hire and contract staffing solutions in the manufacturing and engineering verticals for clients primarily located in the Midwestern U.S. |

|

|

|

|

|

| · | Paladin Consulting primarily provides highly skilled IT professionals on a contract or direct hire basis directly to customers or through resource process outsourcing (“RPO”), managed services provider (“MSP”), and vendor management services (“VMS”) arrangements, and other non-IT staffing solutions to customers nationwide including government contractors who require that the provider of staffing services have top secret (“TS”) clearance; such TS certification is maintained by Paladin Consulting. |

|

|

|

|

|

| · | Scribe Solutions provides hospital and free-standing emergency rooms and physician practices in the Southeastern U.S. with highly trained medical scribes for personal assistant work in connection with EMR. |

|

|

|

|

|

| · | SNI Companies provides human resource solutions, including direct hire and contract staffing, project support and retained search services specializing primarily in the accounting, finance, banking, IT and office support verticals to customers located in major U.S. metropolitan markets, such as Dallas/Fort Worth, Denver, Miami, Tampa, Jacksonville, Boston, Hartford and surrounding areas. SNI Companies’ brands include Accounting Now, Staffing Now®, SNI Banking, SNI Certes®, SNI Energy®, SNI Financial®, and SNI Technology®. |

Industrial Division

|

| · | Triad Staffing provides light industrial contract labor services for all phases of manufacturing and electronic assembly, warehousing, picking, packing and shipping and custodial and general labor operations throughout Ohio. |

Our Strategy

Our business strategy is multi-dimensional and encompasses both organic growth and growth through strategic acquisitions. The main tenants of our strategy are to:

Grow Organically By:

|

| · | Providing innovative solutions for clients delivered through an enhanced and expanded menu of professional services offerings while increasing the penetration of clients in our existing markets for our IT, finance and accounting, healthcare, engineering and office support verticals; |

|

|

|

|

|

| · | Entering other fast growing markets following existing customers who are expanding their operations and cross-selling services by leveraging strategic customer relationships capitalizing on the Company’s national managed services agreements (“MSA”), MSP and VMS relationships; |

|

|

|

|

|

| · | Expanding our geographic footprint into key markets through both virtual and bricks and mortar de novo office openings; |

|

|

|

|

|

| · | Adding recruiting and sales talent to our existing delivery network to obtain new customers and increase the number of placements made to increase revenue; |

| 8 |

| Table of Contents |

|

| · | Increasing scalability and expanding operating margin through continued realization of economies of scale through the on-going process of streamlining back office operations, leveraging regional and national recruiting centers, improving upon per desk production averages and through the elimination of duplicative costs of acquired companies; and |

|

|

|

|

|

| · | Capitalizing on hiring opportunities created by the economic downturn through providing on-demand labor to fill the personnel voids of businesses following corporate America’s reaction to the 2019 novel coronavirus (“COVID-19”) pandemic with shutdowns, layoffs and displacements of professionals, office support staff and blue collar workers. As the economy recovers and companies return to sustained growth, demand for our services is anticipated to accelerate, with a particular focus on IT, E-Commerce and Logistics. |

Growth Through Strategic Acquisitions:

We have historically grown significantly through acquisitions of complementary businesses. We intend to continue to expand our business through strategic acquisitions, subject to refinement of our business plans and management’s ability to identify, acquire and develop suitable acquisition targets in both new and existing desirable service categories. Along with our significant business growth to date, we have built a robust platform with the appropriate infrastructure and scalability, which we believe is necessary to assimilate acquisitions.

We continue to explore opportunities for potential acquisitions in the fragmented staffing industry. Our acquisition strategy includes, but is not limited to, targeting companies or transactions that we believe may have one or more of the following characteristics:

|

| · | A focus on IT specialties and other verticals, including cyber security, government and targets in the professional services sectors; |

|

|

|

|

|

| · | A well-managed business with experienced operators and with high gross and Earnings Before Interest, Taxes, Depreciation, and Amortization (“EBITDA”) margins, as well as consistent revenue growth; |

|

|

|

|

|

| · | Limited enterprise risk and successful due diligence; and |

|

|

|

|

|

| · | Pricing commensurate with profitability and growth, must be accretive to earnings and consideration generally consisting of a combination of cash, seller and bank financing and stock. |

Marketing

We market our staffing services using our corporate and trade names in our respective vertical markets. As of March 1, 2021, we operated 30 branch and virtual locations in downtown or suburban areas of major U.S. cities in eleven states, including one located in each of Connecticut, Georgia, Minnesota, New Jersey, and Virginia, three offices in Colorado, two offices in Illinois and Massachusetts, four offices in Texas, seven offices each in Ohio and Florida.

We market our staffing services to prospective clients primarily through the use of the internet, specialty brands and corporate websites, digital direct mail campaigns, publishing annual electronic and widely distributed salary guides, advertising in tech, HR and accounting publications, attendance and booth displays at specialty trade shows, participation and membership in chambers of commerce, the Society for Information Management (“SIM”), Women in Technology and other business organizations, support for our employees’’ philanthropic activities, telephone marketing by our sales consultants and business development managers using our customer relationship management (“CRM”) tools to identify prospects, and through the electronic mailing of tailored employment bulletins which list highly-skilled candidates available for placement and contract employees available for assignment.

Competition

The staffing industry is highly fragmented with a multitude of competitors. There are relatively few barriers to entry by firms offering direct hire placement and staff augmentation services although significant amounts of working capital typically are required to fund the payroll of temporary workers for businesses providing contract staffing services. New entrants to the staffing industry are constantly introduced to the marketplace. Our competitors include sole-proprietorship operations, local and regional firms as well as national organizations. In the U.S., large national firms have annual revenue of approximately $100 million and up to $10 billion. Regional firms yearly revenue ranges from $10 million or more. The largest portion of the marketplace is the bottom layer of this competitive landscape consisting of small, individual-sized or family-run operations. With low barriers to entry, sole proprietorships and smaller entities routinely enter the staffing industry. Many competitors are larger corporations with substantially greater resources than ours; however, as described below, we believe we are able to compete successfully in the verticals and end markets in which we operate.

| 9 |

| Table of Contents |

Our professional and industrial staffing services compete effectively by providing highly qualified candidates who are well matched for the position, developing and maintaining outstanding client relationships on a local level, responding quickly to client requests, and by establishing offices in convenient locations. As part of our services, we provide professional reference checking, scrutiny of candidates’ work experience and optional custom background checks. In general, we believe that pricing is secondary to quality of service as a competitive factor. During slow hiring periods, however, competition can put pressure on our pricing and we believe we are able to effectively compete on price in such situations.

Our Competitive Strengths

We believe that we are able to compete effectively in the staffing industry because we have:

|

| · | Deep experience and vertical specialization and expertise in niche markets; |

|

|

|

|

|

| · | Invested in robust sales programs and marketing tools and technology and CRM software to successfully target and reach out to potential new customers; |

|

|

|

|

|

| · | Long-tenured division leaders, business development managers and vertical specialists (e.g., certified public accountants for accounting, tax and financial placements) with deep and relevant staffing industry experience; |

|

|

|

|

|

| · | Strong and proven capability to deliver outstanding results upon short notice on large-scale projects leveraging our wide office network and experienced project team leaders, including experience with MSP and VMS programs; |

|

|

|

|

|

| · | Set in place the strategy and procedures for both temporary and permanent virtual working and invested in technology to facilitate communication, recruiting, onboarding and management of the business virtually; |

|

|

|

|

|

| · | Vertical specific state-of-the-art databases, applicant tracking systems (“ATS”) and other technology tools that facilitate swift, expert matching of candidates to job requirements providing highly-qualified multiple choices to customers; |

|

|

|

|

|

| · | Localized decision-making and a lack of a multi-layered bureaucracy which we believe provides for a more rapid response to customized client requests and a streamlined approval process in place for speedy recruitment of personnel; and |

|

|

|

|

|

| · | Hands-on training with specialized modules for newly hired recruiters and account management personnel. |

Recruiting

The success of our services is highly dependent on our ability to recruit and retain qualified candidates. Prospective employment candidates are generally recruited through job postings and contact made electronically using various internet tools as well as telephone contact by our employment consultants. For internet postings, we maintain our corporate web page at www.geegroup.com and our specialty brand web pages in addition to extensive use of internet job posting bulletin board services. We also maintain database records of applicants’ skills through our ATS to assist in matching applicant skills with job openings and contract assignments. We generally screen, interview and, in many cases background check, all applicants who are presented to our clients.

| 10 |

| Table of Contents |

Recent Developments

The COVID-19 Pandemic

COVID-19, which is widely acknowledged as having originated in Wuhan, China over a year ago has since spread throughout the United States and globally. Our business, results of operations, and financial condition have been, and may continue to be, adversely impacted in material respects by the COVID-19 pandemic and related governmental actions (including declared states of emergency and quarantine, “shelter in place” orders, or similar orders), non-governmental organization recommendations, and public perceptions, all of which have led and may continue to lead to disruption in global economic and labor markets. These effects have had a significant impact on our business, including reduced demand for our services and workforce solutions, early terminations or reductions in projects, hiring freezes, and a shift of a significant portion of our workforce to remote operations, all of which have contributed to a decline in revenues and other significant adverse impacts on our financial results. Other potential impacts of the COVID-19 pandemic may include continued or expanded closures or reductions of operations with respect to our client partners’ operations or facilities, the possibility our client partners will not be able to pay for our services or workforce solutions, or that they will attempt to defer payments owed to us, either of which could materially impact our liquidity, the possibility that the uncertain nature of the pandemic may not yield the increase in certain of our workforce solutions that we have historically observed during periods of economic downturn, and the possibility that various government-sponsored programs to provide economic relief may be inadequate. Further, we may continue to experience adverse financial impacts, some of which may be material, if we cannot offset revenue declines with cost savings through expense-related initiatives, human capital management initiatives, or otherwise. As a result of these observed and potential developments, we expect our business, results of operations, and financial condition to continue to be negatively affected.

The ultimate economic impact and duration of the COVID-19 pandemic are difficult to assess or predict and new information about its severity and actions to contain or treat its impact continue to emerge. The COVID-19 pandemic already has caused significant disruptions in general commercial activity throughout the U.S. and global economies and caused financial market volatility and uncertainty. A continuation or worsening of market disruption and volatility could have an adverse effect on our ability to access capital and on the market price of our common stock, and we may not be able to successfully raise needed capital. If we are unsuccessful in raising capital in the future, we may need to reduce activities, curtail or cease operations.

Cares Act Payroll Protection Program Loans

On May 5, 2020, we and certain of our subsidiaries entered into nine (9) unsecured promissory notes (“PPP Loans”) payable under the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) Payroll Protection Program (“PPP”) in order to obtain needed relief funds for allowable expenses under the CARES Act PPP and received net funds totaling approximately $19.9 million. We believe we are eligible for forgiveness of all of our PPP Loans based on existing available guidance and have so far received full forgiveness from the Small Business Administration (“SBA”) for all outstanding principal and interest under the PPP Loan originally made to Scribe Solutions Inc. in the amount of approximately $279 thousand. We are in the process of applying for full forgiveness for our remaining outstanding PPP Loans and related interest. However, there can be no assurance that we will ultimately achieve forgiveness in whole or in part for our remaining outstanding PPP Loans and in that event, would have to repay the unforgiven loan balances in accordance with terms prescribed by the CARES Act.

Amendments to the Revolving Credit, Term Loan and Security Agreement, dated as of March 31, 2017, as amended, amended and restated, restated, supplemented or otherwise modified from time to time (the “Senior Credit Agreement”)

On April 28, 2020, May 5, 2020, June 30, 2020 and December 22, 2020, we entered into the seventh, eighth, ninth and tenth amendments, respectively, to the Senior Credit Agreement (the respective amendments, the “Seventh Amendment,” “Eighth Amendment,” “Ninth Amendment” and “Tenth Amendment”), by and among the Company, Scribe Solutions, Inc., Agile Resources, Inc. Access Data Consulting Corporation, Triad Personnel Services, Inc. Triad Logistics, Inc., Paladin Consulting, Inc., BMCH, INC., GEE Group Portfolio Inc., and SNI Companies, Inc., each a subsidiary of the Company listed as a “Guarantor” on the signature pages thereto each lender named therein and MGG Investment Group LP, as administrative agent, collateral agent and term loan agent for the lenders (“MGG”). The Seventh Amendment contained several features beneficial to us, including an extension of our senior debt maturity for two years, lower cash interest, and postponement and reductions of quarterly principal payments. In exchange, the Company agreed to replace the lower cash interest with pay-in-kind (“PIK”) interest on the term loan portion of its senior debt pursuant to the Senior Credit Agreement to pursue, negotiate, and execute conversions of all of our outstanding subordinated debt and preferred stock into shares of our common stock, and to incur restructuring and exit fees totaling approximately $5.0 million payable in cash or stock to the senior lenders at a future date. The Eighth and Ninth Amendments were entered into enable and provide conforming changes to the Senior Credit Agreement so that the Company could obtain its PPP Loans and complete the repurchases, settlements and/or conversions of all of its subordinated debt and preferred stock outstanding as of June 30, 2020. The Tenth Amendment (the most recent amendment) extended the time to negotiate and settle certain terms of the restructuring and exit fees from September 30, 2020, which was established in the Ninth Amendment, to June 30, 2021, as further described below.

| 11 |

| Table of Contents |

Completion of Financial Restructuring Transactions

On June 30, 2020, we completed a financial restructuring of approximately $19.7 million of our subordinated indebtedness and approximately $27.7 million of our convertible preferred stock (the “Restructuring”) pursuant to the terms of the Seventh Amendment and Ninth Amendment to the Senior Credit Agreement. In connection with the restructuring, we entered into the following agreements with the holders of our subordinated indebtedness and convertible preferred stock.

We entered into a Repurchase Agreement for Preferred Stock and Subordinated Notes (the “Repurchase Agreement”), dated as of June 30, 2020 with Ronald R. Smith (“Mr. Smith”), Thrivent Financial for Lutherans, Madison Capital Funding LLC, Maurice R. Harrison IV, Peter Langlois, Vincent Lombardo and Shane Parr (collectively with Smith, Thrivent and Madison, the “SNI Group Members” pursuant to which the SNI Group Members agreed to allow us to repurchase and settle all of the 9.5% Convertible Subordinated Notes (the “9.5% Notes”), Series B Convertible Preferred Stock, no par value (“Series B Preferred Stock”), 8% Convertible Subordinated Notes (“8% Notes”), and Series C 8% Cumulative Convertible Preferred Stock, no par value (“Series C Preferred Stock”), held by each of them as set forth below. All of the outstanding 9.5% Notes and all of the outstanding Series B Preferred Stock were held by SNI Group Members.

Pursuant to the Repurchase Agreement, the holders of the 9.5% Notes agreed to accept an aggregate amount of approximately $1.1 million in cash in consideration for the purchase by us of the entire $12.5 million aggregate principal amount of the 9.5% Notes held by them. This amount was paid to the SNI Group Members on June 30, 2020.

Pursuant to the Repurchase Agreement the holders of the Series B Preferred Stock agreed to accept an aggregate amount of approximately $2.9 million in cash in consideration for the purchase by us of all 5,565,843 outstanding shares of Series B Preferred Stock held by them. This amount was paid to the SNI Group Members on June 30, 2020.

Pursuant to the Repurchase Agreement, one of the SNI Group members also agreed to accept an aggregate amount of $520 thousand in cash in consideration for the purchase by us of the $1.0 million aggregate principal amount of 8% Notes held by him. Pursuant to the Repurchase Agreement this SNI Group member also agreed to accept an aggregate amount equal to approximately $37 thousand in cash in consideration for the purchase by us of the 71,820 shares of Series C Preferred Stock held by him. These amounts were paid to him on June 30, 2020.

On June 30, 2020, the related party holders of the remaining $1.0 million aggregate principal amount of our 8% Notes converted such 8% Notes into an aggregate of 1,000,000 shares of Series C Preferred Stock which were immediately and simultaneously converted into 1,000,000 shares of common stock at the $1.00 per share conversion price stated in the 8% Notes and in the Series C Preferred Stock. These holders also converted an aggregate of 93,246 additional shares of Series C Preferred Stock issued or issuable to them into a total of 93,246 shares of common stock at the $1.00 per share conversion price stated in the Series C Preferred Stock. The issuance of the 1,093,246 shares of common stock to these former holders of 8% Notes and Series C Preferred Stock was completed on June 30, 2020.

| 12 |

| Table of Contents |

On June 30, 2020, we and Jax Legacy Investment 1, LLC (“Jax Legacy”), the sole holder of our 10% Convertible Subordinated Notes (the “10% Notes”), entered into a Note Conversion Agreement whereby Jax Legacy agreed to immediately convert the approximately $4.2 million aggregate principal amount of 10% Notes held by it into 717,839 shares of common stock at the $5.83 per share conversion rate stated in the 10% Notes. The conversion of the 10% Notes was consummated on June 30, 2020 and the Company issued 717,839 shares of common stock to Jax Legacy on that date.

On June 30, 2020, we and Enoch S. Timothy and Dorothy Timothy (collectively, “Timothy”) entered into a Note Settlement Agreement pursuant to which Timothy agreed to accept an aggregate amount of approximately $89,000 in cash in consideration for the purchase by us of the $1.0 million aggregate principal amount of the Subordinated Promissory Note dated January 20, 2017. This amount was paid to Timothy on June 30, 2020.

In connection with the Repurchase Agreement, we and the SNI Group Members entered into a Registration Rights Agreement dated as of June 30, 2020 (the “Registration Rights Agreement”). Pursuant to the terms of the Registration Rights Agreement, we agreed to file a registration statement with respect to the resale of shares of common stock currently owned by the SNI Group members that are “Registrable Securities” (as defined in the Registration Rights Agreement). In addition, we agreed that we shall, on one occasion, on or after September 30, 2020 and upon the written request of the holders of 51% or more of the Registrable Securities, file a registration statement with respect to the Registrable Securities held by such holders. The demanding holders may require, in connection with the second registration, that such demand registration take the form of an underwritten public offering of such Registrable Securities. The Registration Rights Agreement also provides that for a period of three years after the closing date of the Restructuring, the holders of Registrable Securities shall have piggyback registration rights with respect to all registration statements filed by the Company (other than those on Form S-4 or Form S-8).

Obligation to Pay Exit and Restructuring Fees Pursuant to Senior Credit Agreement

Pursuant to the Senior Credit Agreement, as amended, we are obligated to pay a total of approximately $5.0 million in Exit and Restructuring Fees (the “Exit and Restructuring Fees”) in cash or in shares of our common stock, as determined in the sole discretion of MGG, on or prior to June 30, 2021. We have been informally advised by MGG that it intends to seek payment of these fees in shares of common stock. Pursuant to the Senior Credit Agreement, the shares of common stock to be issued shall be valued at $1.00 per share which would result in the issuance of 4,978,197 shares of common stock on or prior to June 30, 2021. We expect that these shares of common stock (if MGG elects to receive common stock) will be issued pursuant to an exemption from registration under the Securities Act and the refore MGG’s re sale of such common stock will be restricted absent an effective registration statement or an exemption from registration pursuant to the Securities Act. Pursuant to our agreement with MGG, we are required to file a registration statement to register the resale of these shares.

Entry into a Commitment Letter with CIT

On March 22, 2021, we signed a commitment letter (the “Commitment Letter”) for a $20 million asset-based senior secured revolving credit facility (the “CIT Facility”) with CIT Bank, N.A. (“CIT”), who will also serve as administrative and collateral agent and sole lead arranger. The CIT Facility will be collateralized by 100% of our assets and those of our subsidiaries who will act as co-borrowers and guarantors. The CIT Facility will have a term that matures at the earlier of 180 days prior to the maturity date of the existing term loan or any indebtedness that refinances such term loan and the fifth anniversary of the closing date. Once closed, the CIT Facility will replace our current asset-based lending credit facility.

Under the CIT Facility, advances will be subject to a borrowing base formula that will be computed based on 85% of our eligible accounts receivable and subsidiaries in general and as further defined in the loan documents, and subject to certain other criteria, conditions and applicable reserves, including any additional eligibility requirements as determined by the administrative agent. The CIT Facility will be subject to usual and customary covenants and events of default for credit facilities of this type. The interest rate, at our election, will be based on either the Base Rate, as defined, plus the applicable margin; or, the London Interbank Offering Rate (“LIBOR,” or any successor thereto) for the applicable interest period, subject to a 1% floor, plus the applicable margin. Based upon our anticipated amount of borrowings under the CIT Facility, the estimated effective interest rate is expected to be in the range of approximately 4% to approximately 5.25%, based on the three months LIBOR rate as of March 26, 2021. This compares to an approximately 11% interest rate currently paid on the Company’s present ABL. In addition to interest costs on advances outstanding, the CIT Facility will provide for an unused line fee ranging from 0.375% to 0.50% depending on the amount of undrawn credit, original issue discount and certain fees for diligence, implementation and administration.

Closing of the CIT Facility is subject to the completion of a satisfactory field examination and due diligence, compliance with the required closing conditions, execution of an acceptable inter-creditor agreement if term debt remains outstanding and finalization of definitive documentation.

Our Corporate Information

We were incorporated in the State of Illinois in 1962 and are the successor to employment offices doing business since 1893. Our principal executive offices are located at 7751 Belfort Parkway, Suite 150, Jacksonville, Florida 32256, and our telephone number at that location is (630) 954-0400. Our Internet website address is www.GEEgroup.com. The inclusion of our website address in this prospectus does not include or incorporate by reference into this prospectus or the registration statement to which it forms a part any information on, or accessible through, our website.

Summary of Risk Factors

Our business is subject to numerous risks and uncertainties that you should consider before investing in our company. You should carefully consider the risks described more fully in the section titled “Risk Factors” in this prospectus beginning on page 18, before making a decision to invest in our common stock. If any of these risks actually occur, our business, financial condition and results of operations would likely be materially adversely affected. These risks, include, but are not limited to, the following:

|

| · | We have experienced losses from operations and may not be profitable in the future. |

|

|

|

|

|

| · | The terms of our Senior Credit Agreement place restrictions on our operating and financial flexibility, and failure to comply with covenants or to satisfy certain conditions of the agreement may result in acceleration of our repayment obligations, which could significantly harm our liquidity, financial condition, operating results, business and prospects and cause the price of our securities to decline. The covenants contained in our Senior Credit Agreement also include the requirement that we maintain specific financial ratios. If we cannot comply with these covenants, we also may be in default under the credit agreement. |

|

|

|

|

|

| · | Recent global socioeconomic trends, including the negative effects of the COVID-19 pandemic, and trends in the financial markets could adversely affect our business, liquidity and financial results. |

|

|

|

|

|

| · | If we are unable to generate or borrow sufficient cash to make payments on our indebtedness, including any unforgiven portion of our PPP Loans, our financial condition would be materially harmed, our business could fail and our shareholders may lose all of their investment. |

| 13 |

| Table of Contents |

|

| · | We have material intangible assets, including goodwill, customer lists, trademarks and tradenames. These assets are subject to impairment risks, which could result in future material impairment charges to income and negatively impacting the future operating results and our financial position. |

|

|

|

|

|

| · | We have significant working capital needs and if we are unable to satisfy those needs from cash generated from our operations or borrowings, we may not be able to continue our operations. |

|

|

|

|

|

| · | Our revenue can vary because our customers can terminate their relationship with us at any time with limited or no penalty. |

|

|

|

|

|

| · | If we are unable to retain a broad group of existing customers, lose one or more significant customers, or fail to attract new customers, our results of operations could suffer. |

|

|

|

|

|

| · | Substantial alteration of our current business and revenue model could hurt our results. |

|

|

|

|

|

| · | We depend on our senior management team and the loss of one or more key employees or an inability to attract and retain highly skilled employees could adversely affect our business. |

|

|

|

|

|

| · | We depend on attracting, integrating, managing, and retaining qualified internal personnel. |

|

|

|

|

|

| · | We depend on our ability to attract and retain qualified temporary workers. |

|

|

|

|

|

| · | We operate in an intensely competitive and rapidly changing business environment, and there is a substantial risk that our services could become obsolete or uncompetitive. |

|

|

|

|

|

| · | We may not be able to compete successfully with our existing and potential competitors. |

|

|

|

|

|

| · | We may not be able to manage expected growth and internal expansion. |

|

|

|

|

|

| · | Our strategy of growing through acquisitions may be impeded by a lack of financial resources and impact our business in unexpected ways. We could be adversely affected by risks associated with acquisitions. |

|

|

|

|

|

| · | We may not be able to obtain the necessary capital or additional capital or financing to achieve our strategic goals. |

|

|

|

|

|

| · | Changes in government regulation could limit our growth or result in additional costs of doing business. |

|

|

|

|

|

| · | We are dependent upon technology services, and if we experience damage, service interruptions or failures in our computer and telecommunications systems, our existing customer relationships and our ability to attract new customers may be adversely affected. |

|

|

|

|

|

| · | We could be harmed by improper disclosure or loss of sensitive or confidential company, employee, associate or customer data, including personal data. |

|

|

|

|

|

| · | Our ability to utilize our net operating carryforwards and certain other tax attributes may be limited. |

|

|

|

|

|

| · | We may be exposed to employment-related claims and losses, including class action lawsuits, which could have a material adverse effect on our business. |

|

|

|

|

|

| · | The requirements of being a public company may strain our financial and human resources and distract management. |

|

|

|

|

|

| · | We may be unable to implement and maintain appropriate internal controls over financial reporting. If we fail to maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results and current and potential shareholders may lose confidence in our financial reporting. |

|

|

|

|

|

| · | There are inherent limitations in all control systems, and misstatements due to error or fraud may occur and not be detected. |

|

|

|

|

|

| · | Our operations may be affected by domestic and global economic fluctuations. |

|

|

|

|

|

| · | Interruption of our business could result from increased security measures in response to terrorism. |

|

|

|

|

|

| · | Our business may be impacted by political events, war, public health issues, inclement weather, natural disasters and other business interruptions. |

|

|

|

|

|

| · | The market price of shares of our common stock has been volatile, which could cause the value of your investment to decline. A more active, liquid trading market for our common stock may not develop, and the price of our common stock may fluctuate significantly. |

| 14 |

| Table of Contents |

|

| · | Our common stock could be delisted from the NYSE American if we do not meet its continued listing requirements. |

|

|

|

|

|

| · | We have no current plans to pay cash dividends on our common stock; as a result, you may not receive any return on investment unless you sell your common stock for a price greater than that which you paid for it. |

|

|

|

|

|

| · | You will experience immediate and substantial dilution if you purchase securities in this offering. |

|

|

|

|

|

| · | There may be future sales of our securities or other dilution of our equity, which may adversely affect the market price of our common stock. |

|

|

|

|

|

| · | Our compliance with complicated regulations concerning corporate governance and public disclosure has resulted in additional expenses. |

|

|

|

|

|

| · | Provisions in our amended and restated articles of incorporation, as amended, our amended and restated by-laws, as amended, and Illinois law might discourage, delay or prevent a change in control of our company or changes in our management and, therefore, depress the trading price of our common stock. |

|

|

|

|

|

| · | If securities or industry analysts do not publish or cease publishing research or reports about us, our business or our market, or if they change their recommendations regarding our stock adversely, our stock price and trading volume could decline. |

|

|

|

|

|

| · | Our management will have broad discretion over the use of the proceeds we receive in this offering and might not apply the proceeds in ways that increase the value of your investment. |

|

|

|

|

|

| · | A possible “short squeeze” due to a sudden increase in demand of our common stock that largely exceeds supply may lead to further price volatility in our common shares. |

Implications of Being a Smaller Reporting Company

We are a “smaller reporting company” and accordingly may provide less public disclosure than larger public companies, including the inclusion of only two years of audited consolidated financial statements and only two years of management’s discussion and analysis of financial condition and results of operations disclosure. As a result, the information that we provide to our shareholders may be different than you might receive from other public reporting companies in which you hold equity interests.

| 15 |

| Table of Contents |

| Common stock offered by us | 31,250,000 shares |

|

|

|

| Common stock to be outstanding immediately after this offering (excluding over-allotment option) 1 | 53,895,320 shares |

|

|

|

| Over-allotment option | 4,687,500 shares |

|

|

|

| Use of proceeds | We expect to receive net proceeds from the sale of shares of our common stock in this offering of approximately $45,495,000, based on an assumed public offering price of $1.60 per share, the last reported sale price of our common stock on the NYSE American on March 26, 2021, and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. If the underwriters exercise their option to purchase additional shares of common stock, we estimate that we will receive an additional $6,938,000 net proceeds. We intend to use the net proceeds of this offering, together with the CIT Facility and available cash and/or common stock to repay approximately $59,999,000 in aggregate, of outstanding indebtedness under the Senior Credit Agreement and the remainder, if any, for general corporate purposes, including working capital and potential acquisitions. See “Use of Proceeds” on page 35.

|

| NYSE American trading symbol

| “JOB” |

| Risk factors | The securities offered by this prospectus are speculative and involve a high degree of risk and investors purchasing securities should not purchase the securities unless they can afford the loss of their entire investment. See “Risk Factors” beginning on page 18. |

|

|

|

| Lock-Up | We, each of our directors and Section 16(b) officers, and any other 5% or greater holder (with the exception of institutional and mutual fund holders) of our outstanding shares of common stock have agreed not to sell, offer, agree to sell, contract to sell, hypothecate, pledge, grant any option to purchase, make any short sale of, or otherwise dispose of or hedge, directly or indirectly, any shares of our capital stock or any securities convertible into or exercisable or exchangeable for shares of capital stock, for a period of (i) six (6) months after the date of this prospectus in the case of our directors and Section 16(b) officers and (ii) three (3) months after the date of this prospectus in the case of the Company and 5% or greater holder (with the exception of institutional and mutual fund holders) of outstanding shares, without the prior written consent of the representative of the underwriters. See “Underwriting” for additional information. |

1 The number of shares of our common stock to be outstanding immediately after this offering is based on 17,667,123 shares of common stock outstanding as of March 26, 2021, and includes (i) 31,250,000 common shares being offered by us in this offering, and (ii) 4,978,197 common shares which may be issued to MGG pursuant to our Senior Credit Agreement in settlement of certain accrued and unpaid fees on or before June 30, 2021, and excludes:

|

| · | 1,304,572 shares of common stock issuable upon the exercise of outstanding options and warrants at a weighted average exercise price of $2.75 per share; |

|

|

|

|

|

| · | 1,450,000 shares of common stock issuable upon the vesting of restricted stock units, of which 600,000 shares are scheduled to vest on June 15, 2021; and |

|

|

|

|

|

| · | 3,334,000 shares of common stock reserved for issuance under our 2013 Amended and Restated Incentive Stock Plan . |

Unless otherwise stated, all information in this prospectus assumes no exercise of the underwriters’ over-allotment option to purchase additional shares of common stock.

| 16 |

| Table of Contents |

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following table presents our summary historical financial data for the periods presented and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included elsewhere in this prospectus. The statements of operations data for the fiscal years ended September 30, 2020 and 2019 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary unaudited consolidated statements of operations data for the three months ended December 31, 2020 and 2019 and the consolidated balance sheet data as of December 31, 2020 have been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. You also should read this data together with the information under the captions “Capitalization” and “Dilution.” Our historical results are not necessarily indicative of our future results or any other period. The summary financial data included in this section are not intended to replace the financial statements and the related notes included elsewhere in this prospectus.

|

|

| Three Months Ended December 31, |

|

| Year Ended September 30, |

| ||||||||||

|

|

| 2020 |

|

| 2019 |

|

| 2020 |

|

| 2019 |

| ||||

| (Dollars and shares in thousands, except per share amounts) |

| (unaudited) |

|

| (unaudited) |

|

|

|

|

|

|

| ||||

| Consolidated Statements of Operations Data: |

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Net revenues |

| $ | 34,643 |

|

| $ | 37,557 |

|

| $ | 129,835 |

|

| $ | 151,674 |

|

| Gross profit |

|

| 12,580 |

|

|

| 12,595 |

|

|

| 44,704 |

|

|

| 52,021 |

|

| Selling, general and administrative expenses |

|

| 9,487 |

|

|

| 11,291 |

|

|

| 44,401 |

|

|

| 46,739 |

|

| Depreciation and amortization |

|

| 1,117 |

|

|

| 1,477 |

|

|

| 5,286 |

|

|

| 5,935 |

|

| Goodwill impairment charge |

|

| - |

|

|

| - |

|

|

| 8,850 |

|

|

| 4,300 |

|

| Income (loss) from operations |

|

| 1,976 |

|

|

| (173 | ) |

|

| (13,833 | ) |

|

| (4,953 | ) |

| Gain on extinguishment of debt |

|

| - |

|

|

| - |

|

|

| 12,316 |

|

|

| - |

|

| Interest expense |

|

| (2,686 | ) |

|

| (3,219 | ) |

|

| (12,233 | ) |

|

| (12,440 | ) |

| Net income (loss) |

|

| (315 | ) |

|

| (3,563 | ) |

|

| (14,347 | ) |

|

| (17,763 | ) |

| Gain on redeemed preferred stock |

|

| - |

|

|

| - |

|

|

| 24,475 |

|

|

| - |

|

| Net income (loss) attributable to common shareholders |

| (315) |

|

| (3,563) |

|

| 10,128 |

|

| (17,763) |

| ||||

| Basic earnings (loss) per share |

| (0.02) |

|

| (0.27) |

|

| 0.67 |

|

| (1.50) |

| ||||

| Diluted earnings (loss) per share |

| $ | (0.02) |

|

| $ | (0.27) |

|

| $ | (1.14) |

|

| $ | (1.50) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Weighted average number of shares: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

| 17,667 |

|

|

| 13,067 |

|

|

| 15,214 |

|

|

| 11,840 |

|

| Diluted |

|

| 17,667 |

|

|

| 13,067 |

|

|

| 21,570 |

|

|

| 11,840 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Unaudited pro forma net income (loss) per share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pro forma net income attributable to common shareholders (1) |

| $ | 2,206 |

|

|

|

|

|

| $ | 19,945 |

|

|

|

|

|

| Pro forma net income per share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

| $ | 0.04 |

|

|

|

|

|

| $ | 0.39 |

|

|

|

|

|

| Diluted |

| $ | 0.04 |

|

|

|

|

|

| $ | (0.25) |

|

|

|

|

|

| Weighted average number of shares (2): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

| 53,895 |

|

|

|

|

|

|

| 51,442 |

|

|

|

|

|

| Diluted |

|

| 55,345 |

|

|

|

|

|

|

| 57,798 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Dollars in thousands) |

|

|

|

|

|

|

|

|

| As of December 31, 2020 |

| |||||

|

|

|

|

|

|

|

|

|

|

| Actual |

|

| Pro Forma (2) |

| ||

| Consolidated Balance Sheet Data: |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

| Cash (3) |

|

|

|

|

|

|

|

|

| $ | 14,119 |

|

| $ | 14,593 |

|

| Total current assets (3) |

|

|

|

|

|

|

|

|

|

| 33,593 |

|

|

| 34,067 |

|

| Total assets (3) |

|

|

|

|

|

|

|

|

|

| 120,471 |

|

|

| 120,945 |

|

| Total current liabilities (4) |

|

|

|

|

|

|

|

|

|

| 22,108 |

|

|

| 17,130 |

|

| Total long-term liabilities (5) |

|

|

|

|

|

|

|

|

|

| 70,989 |

|

|

| 30,417 |

|

| Total liabilities (4) (5) |

|

|

|

|

|

|

|

|

|

| 93,097 |

|

|

| 47,547 |

|

| Total shareholders’ equity (6) |

|

|

|

|

|

|

|

|

| $ | 27,374 |

|

| $ | 73,398 |

|

| (1) | The unaudited pro forma net income gives effect to the reduction in interest expense due to the expected pay-off, settlement and retirement of all amounts due under the Senior Credit Agreement (see “Use of Proceeds” for additional information), offset by the interest expense on borrowings under the CIT Facility (net decrease in interest expense is $2,521 and $9,817 for the three months ended December 31, 2020 and for the year ended September 30, 2020, respectively). Amortization of debt discount of $4,449 is not included in pro forma net income due to not having a continuing effect on the operating results of the Company. |

|

|

|

| (2) | The share amounts used to calculate unaudited pro forma net income per share reflects issuance and sale of 31,250 shares of our common stock in this offering (based on the assumed offering price), with the net proceeds being used to repay all the amounts due under the Senior Credit Agreement, and also give effect to the issuance of 4,9 78 shares of the Company’s common stock in settlement of Exit and Restructuring Fees pursuant to the terms of the Senior Credit Agreement. Pursuant to the terms of Senior Credit Agreement, we are obligated to pay a total of approximately $4,978 in Exit and Restructuring Fees in cash or in shares of our common stock, as determined in the sole discretion of our senior lenders, on or prior to June 30, 2021. We have been informally advised on behalf of our senior lenders that they intend to seek payment of these fees in shares of common stock. Pursuant to the Senior Credit Agreement, the shares of common stock to be issued are to be valued at $1.00 per share which would result in the issuance of 4,978 shares of common stock on or prior to June 30, 2021. We expect that these shares of common stock (if MGG elects to receive common stock) will be issued pursuant to an exemption from registration under the Securities Act and therefore MGG’s resale of such common stock will be restricted absent an effective registration statement or an exemption from registration pursuant to the Securities Act. Pursuant to our agreement with MGG, we are required to file a registration statement to register the resale of these shares. |

| 17 |

| Table of Contents |

The share amounts used to calculate pro forma net income per common share, basic and diluted, set forth in the table assume no exercise of the underwriters’ over-allotment option to purchase additional shares of common stock, and also exclude:

|

| · | 1,305 shares of common stock issuable upon the exercise of outstanding options and warrants at a weighted average exercise price of $2.75 per share; |

|

|

|

|

|

| · | 1,450 shares of common stock issuable upon the vesting of restricted stock units; of which 600,000 shares are scheduled to vest on June 15, 2021; and |

|

|

|

|

|

| · | 3,334 shares of common stock reserved for issuance under our 2013 Amended and Restated Incentive Stock Plan. |

| (3) | Pro forma cash, total current assets and total assets as of December 31, 2020 give effect to the residual cash, after the transactions described in notes (1) and (2), of $474. |

|

|

|

| (4) | Pro forma current liabilities as of December 31, 2020, give effect to the settlement of the $4,978 in Exit and Restructuring Fees discussed in footnote 2. |

|

|

|

| (5) | Pro forma long-term liabilities as of December 31, 2020, give effect to (i) the pay-off, settlement and retirement of all amounts due under the Senior Credit Agreement, in the aggregate amount of approximately $55,021, using a combination of the net cash proceeds of this offering in the amount of $45,495 and write off of debt discount of $4,449, combined with assumed borrowings under a new collateralized senior bank asset-based revolving credit facility of $10,000 and/or available cash, and (ii) settlement of the $4,978 in Exit and Restructuring Fees discussed in footnotes (2) and (4). |

|

|

|

| (6) | The pro forma total shareholders’ equity gives effect to (i) the net proceeds of this offering in the aggregate amount of $45,495, after deducting the 7.5% underwriting discount, and estimated expenses associated with this offering of approximately $4,505, (ii) the issuance of 4,978 shares of common stock at $1.00 per share pursuant to the Senior Credit Agreement, as discussed in footnote 2, and (iii) a charge to eliminate unamortized debt costs in the amount of $4,449 as of December 31, 2020. |

Non-GAAP Financial Measures

In addition to the Company’s consolidated financial statements presented on a GAAP basis, management uses adjusted EBITDA, which is a supplemental non-GAAP financial measure to provide an additional measure of operating performance. We believe that adjusted EBITDA provides an additional measure for purposes of evaluating the Company’s performance period over period, analyzing the underlying operating trends in the Company’s business, establishing operational goals, and for internal planning, including assessing the Company’s ability to meet debt service and debt financial covenants, make capital expenditures and provide for working capital needs. We define adjusted EBITDA as net income or net loss before interest, taxes, depreciation and amortization plus or minus non-cash stock options and stock-based compensation expenses, acquisition, integration and restructuring costs, certain other non-cash or non-recurring charges, and other gains and losses.

The following table presents the Company’s reconciliation of consolidated net income (loss) to adjusted EBITDA.

Reconciliation of Non-GAAP Adjusted EBITDA to GAAP Net Loss

| (in thousands) |

| Three Months Ended December 31, 2020 |

|

| Year Ended September 30, 2020 |

| ||||||||||

|

|

| 2020 |

|

| 2019 |

|

| 2020 |

|

| 2019 |

| ||||

|

Net income (loss) |

| $ | (315 | ) |

| $ | (3,563 | ) |

| $ | (14,347 | ) |

| $ | (17,763 | ) |

| Interest expense |

|

| 2,686 |

|

|

| 3,219 |

|

|

| 12,233 |

|

|

| 12,440 |

|

| Income taxes |

|

| (395 | ) |

|

| 171 |

|

|

| 597 |

|

|

| 370 |

|

| Amortization and depreciation |

|

| 1,117 |

|

|

| 1,477 |

|

|

| 5,286 |

|

|

| 5,935 |

|

| Non-cash stock compensation |

|

| 311 |

|

|

| 597 |

|

|

| 1,559 |

|

|

| 2,186 |

|

| Acquisition, integration & restructuring, and other gains or losses |

|

| 142 |

|

|

| 377 |

|

|

| 4,277 |

|

|

| 4,281 |

|

| Non-cash goodwill impairment charge |

|

| - |

|

|

| - |

|

|

| 8,850 |

|

|

| 4,300 |

|

| Gain on extinguishment of debt |

|

| - |

|

|

| - |

|

|

| (12,316 | ) |

|

| - |

|

|

Adjusted EBITDA |

| $ | 3,546 |

|

| $ | 2,278 |

|

| $ | 6,139 |

|

| $ | 11,749 |

|

We believe investors also use EBITDA and adjusted EBITDA as supplemental measures to monitor the Company’s performance, including for comparative purposes with other entities and valuation purposes. Generally, a non-GAAP financial measure, such as adjusted EBITDA, is a numerical measure of a company’s performance, financial position or cash flow that either excludes or includes amounts that are not normally excluded or included, accordingly, in the most directly comparable measure calculated and presented in accordance with GAAP. Adjusted EBITDA is not a term defined by GAAP and, as a result, the Company’s measure of adjusted EBITDA might not be comparable to similarly titled measures used by other companies. Adjusted EBITDA, therefore, should be considered in addition to, and not as superior to or as a substitute for, net income or net loss in the Company’s consolidated statements of operations or other measures of financial performance prepared in accordance with GAAP included in our Quarterly Reports on Form 10-Q and Annual Report on Form 10-K filed for the respective fiscal periods with the SEC.

| 18 |

| Table of Contents |

An investment in our securities involves a high degree of risk. Before deciding whether to invest in our securities, you should consider carefully the risks described below, together with other information in this prospectus and in any free writing prospectus that we have authorized for use in connection with this offering. Our business, financial condition, results of operations or cash flow could be seriously harmed as a result of these risks. This could cause the trading price of our common stock to decline, resulting in a loss of all or part of your investment. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us, or that we currently see as immaterial, may also harm our business. Please also read carefully the section below entitled “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Business and Financial Condition

We have experienced losses from operations and may not be profitable in the future.

We incurred consolidated net losses of approximately ($14.3) million and approximately ($17.8) million for the years ended September 30, 2020 and 2019, respectively, and reported consolidated net losses of approximately ($315) thousand for the three months ended December 31, 2020, as compared with approximately ($3.6) million for three months ended December 31, 2019, respectively. Among the consequences of the net losses incurred, the Company has been required to negotiate and obtain concessions from its lenders, including amendments and waivers for missed covenants, under its Senior Credit Agreement. Other possible consequences of recurring net losses include, but are not limited to, negative cash flows, asset impairments, defaults under the Company’s debt agreements, and possibly, the inability of the Company to continue operating as a going concern. Management has taken definitive actions to improve operations, reduce costs and improve operating profitability, and position the Company for future growth. The Company also is actively seeking replacement financing with a view towards reducing its borrowing costs and improving its net cash flow and overall financial profile. However, there are no assurances that the Company will be able to generate sufficient revenue to meet its operating expenditures or operate profitably in the future.